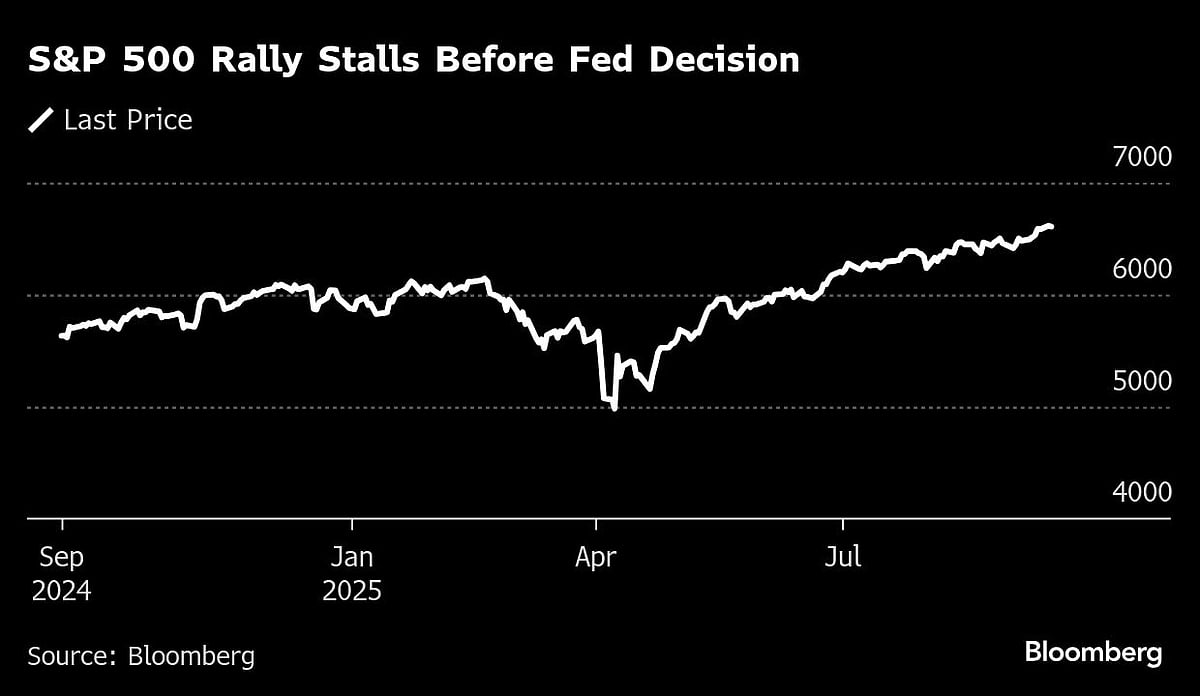

Asian stocks posted a modest drop at the open following a tepid Wall Street session, as investors held back ahead of Wednesday’s Federal Reserve interest-rate decision.

Shares in Japan and South Korea retreated while the MSCI Asia Pacific Index edged 0.2% lower after nine consecutive days of gains. The S&P 500 slipped 0.1% Tuesday and the Nasdaq 100 ended a nine-day winning streak. Equity-index futures for the US posted a small gain.

Gold traded around the $3,700-an-ounce level, after briefly breaching the mark in the prior session buoyed by a softer dollar. A gauge of the greenback edged lower Wednesday, hovering around levels last seen in March 2022. Attention in Asia will also be on a 20-year government bond auction in Japan as political uncertainty and lingering fiscal risks keep longer-dated debt under pressure.

A solid reading on US retail sales Tuesday did little to sway markets, with attention firmly on the Fed meeting. Investors are looking for clues on the path of interest rates that will shape the outlook in the months ahead, with some bond traders stepping up options wagers that the central bank will deliver at least one half-point cut.

“Markets remain in somewhat of a holding pattern ahead of the Federal Reserve’s decision tonight,” wrote Josh Gilbert, a market analyst at eToro in Sydney. “The biggest risk is that the Fed sounds less dovish than markets are hoping for.”

While Fed officials are still focused on bringing inflation to their target, they’re widely expected to cut rates in an effort to shield the labor market from further deterioration.

This is a modal window.

The media could not be loaded, either because the server or network failed or because the format is not supported.

The value of retail purchases, not adjusted for inflation, increased 0.6% after a similar gain in July.

The control-group sales — which feed into the calculation of goods spending for gross domestic product — climbed 0.7%, indicating a healthy quarter.

“Even if the job market is weak, it’s not hurting the consumer yet,” said David Russell at TradeStation. “While these numbers won’t prevent the Fed from cutting rates tomorrow, they reduce some of the longer-term dovish hopes.”

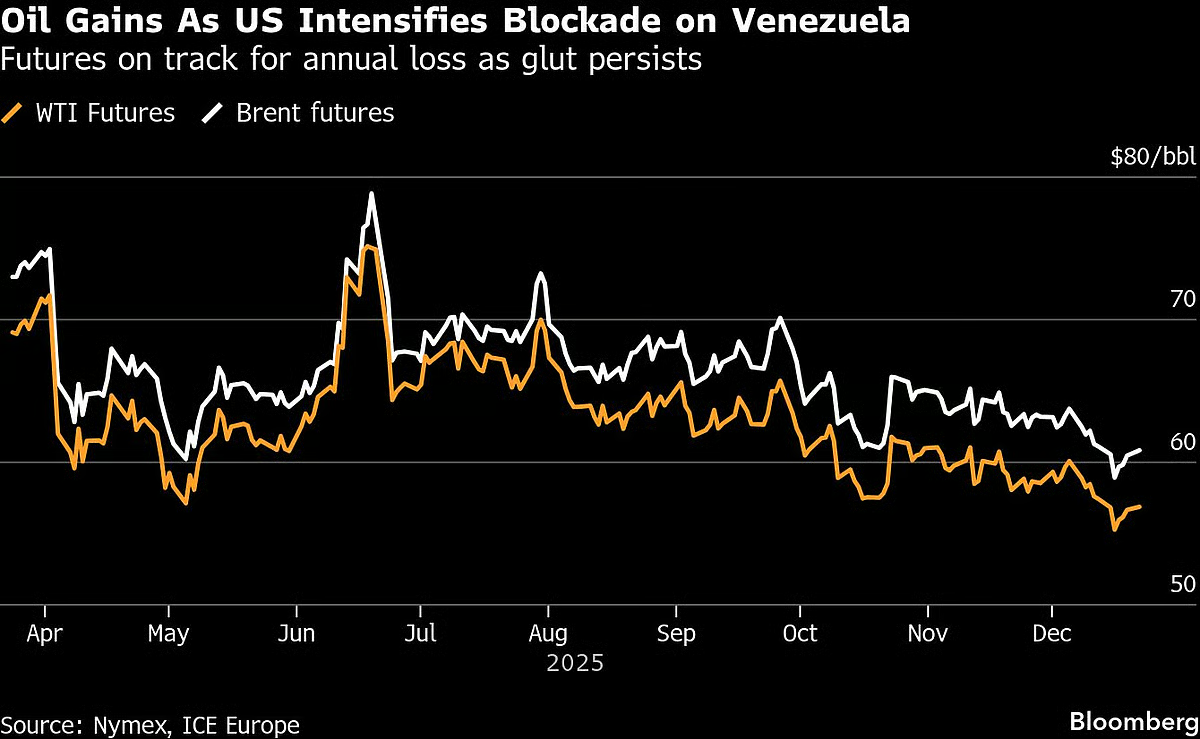

Treasuries held gains after a solid sale of 20-year bonds. The yield on two-year notes slid three basis points to 3.50%. The euro hit its highest since 2021, while the yen touched its strongest mark in a month. Oil rose as pressure mounted on Russia and the conflict in the Middle East flared up.

While the retail-sales report was another piece of good economic news, much of the recent stock rally has been driven by expectations of six rate cuts over the next 12 months, according to Florian Ielpo at Lombard Odier Investment Managers.

“These six cuts can only come if the job-market deterioration is material and the equity performance that came with it is dependent over it,” he said.

Investors will look for changes in the latest quarterly rates projections, known as the dot plot, and pore over Chair Jerome Powell’s remarks later.

Recent speculation about the need for a 50-basis-point rate cut is not justified by the current data, according to Seema Shah at Principal Asset Management. Broader economic indicators — including earnings and credit spreads — do not reflect the kind of deterioration typically warranting that level of action, she said.

“We join the chorus of voices anticipating a 25-basis-point Fed cut,” said Lauren Goodwin at New York Life Investments. “That said: though we expect the market reaction to the Fed meeting to have a ‘sell the news’ flavor, we’d fade that pessimism in the near term.”

Money markets are fully pricing in a quarter-point Fed reduction, and a series of interest-rate cuts over the next year. An outlook echoing that view would be an encouraging sign for stock bulls, who have largely banked on a gradual easing path that keeps the economy from sliding into a recession.

Corporate Highlights:

-

Tencent Holdings Ltd. raised 9 billion yuan ($1.27 billion) on Tuesday from its first bond sale in four years.

-

Chery Automobile Co. is seeking to raise as much as HK$9.1 billion ($1.2 billion) in a Hong Kong initial public offering, kicking off what’s shaping up to be a busy season for big listings in the financial hub.

-

Microsoft Corp., OpenAI and other American companies announced plans to spend tens of billions of dollars on technology infrastructure in the UK, part of a series of business deals that coincide with President Donald Trump’s visit to the nation this week.

Key Events This WeekFor top events, click here.

Some of the main moves in markets:

Stocks

-

S&P 500 futures were little changed as of 9:27 a.m. Tokyo time

-

Hang Seng futures rose 0.6%

-

Japan’s Topix fell 0.9%

-

Australia’s S&P/ASX 200 fell 0.3%

-

Euro Stoxx 50 futures rose 0.3%

Currencies

-

The Bloomberg Dollar Spot Index was little changed

-

The euro was little changed at $1.1868

-

The Japanese yen rose 0.1% to 146.29 per dollar

-

The offshore yuan was little changed at 7.1018 per dollar

-

The Australian dollar was little changed at $0.6688

Cryptocurrencies

-

Bitcoin fell 0.1% to $116,774.17

-

Ether rose 0.4% to $4,517.16

Bonds

-

The yield on 10-year Treasuries was little changed at 4.02%

-

Japan’s 10-year yield advanced one basis point to 1.605%

-

Australia’s 10-year yield was little changed at 4.22%

Commodities

-

West Texas Intermediate crude was little changed

-

Spot gold was little changed

This story was produced with the assistance of Bloomberg Automation.

. Read more on Markets by NDTV Profit.Shares in Japan and South Korea retreated while the MSCI Asia Pacific Index edged 0.2% lower after nine consecutive days of gains. Read MoreMarkets, Business, Notifications, Bloomberg NDTV Profit