Following a robust 18% surge in its stock price so far in 2025, Reliance Industries is firmly in the spotlight, attracting varied perspectives from leading brokerages.

While analysts are broadly optimistic, citing strong growth visibility across its telecom and retail ventures and a recovery in the energy segment, the consensus is clear: the conglomerate’s growth phase is re-accelerating.

With two significant target price hikes from Bernstein and JP Morgan against a minor trim by Jefferies, the market is closely watching to see if the company’s attractive valuation will lead to a further re-rating.

Jefferies On Relinace Industries

While Jefferies maintained its buy call on Reliance Industries, it marginally trimmed its target to Rs 1,650 per share.

The brokerage defined the rationale behind its bullish view to be improving growth visibility on space addition in Retail, constructive tariff outlook in Jio, strong showing in O2C in Q1

The company currently trades below its long term average EV/Ebitda valuations based on projected earnings, which could allow for re-rating.

With the focus back on growth, and streamlining largely behind, the conglomerate’s retail segment resumed healthy mid-teens growth in quarter ended March, 2025, driven by same store sales growth improvement.

Its foray into quick commerce has also seen healthy traction, with plans to substantially expand ahead.

Jio remains well-placed to deliver 18% compounded growth in revenue over FY25-27 and 21% compounded Ebitda growth over the same period

Growth to be supported by improving pricing environment, and scale-up of home broadband business

Healthy growth outlook with moderating capital expenditure will lead to as much as a tenfold rise in free cash flows over the two year period

According to Jefferies, the telecommunication sector is the best way to play the consumption theme in India, which further supports its rationale for a likely re-rating in the company’s valuations.

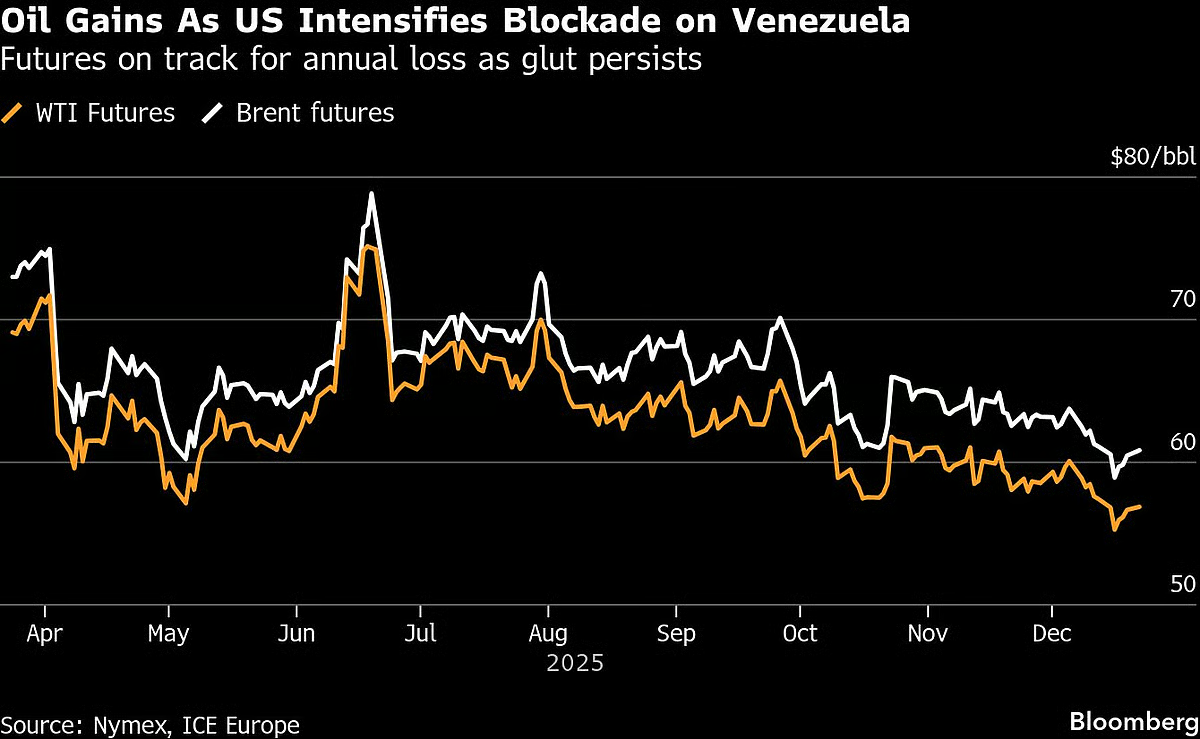

In calendar year 2025 so far, permanent refinery closures have totaled up to 1.1mmbpd or million barrels per day. This has been more than what was closed over 2023 and 2024, combined.

With net refinery capacity additions lower than the projected demand growth, this should benefit the company’s margins.

Petchem spreads are now gradually recovering from the lowest level in a decade hit in Q3FY25, the Jefferies note said, and while the outlook remains soft, a further downside could be limited.

Reliance Industries: Bear Case Scenario

Jefferies also considered a downside scenario with a price target of Rs 1150 implying a 19% downside. Potential triggers for such a scenario could be lower-than-expected telecom ARPU or subscribers for Jio, which could lead to a valuation derating.

Further, a slower recovery in China could also lead to lower margins in the refining/petchem segment.

An elevated cash burn in e-commerce leading a valuation derating could also lead to the downside scenario.

In its base case scenario however, the brokerage projects an upside of 16%.

Bernstein On Reliance Industries

Bernstein maintained an outperform rating, and raised its target price to Rs 1,640 (earlier Rs 1520), implying a 15% upside.

The brokerage sees growth momentum strengthening on the back of store rationalization nearing completion, continued tariff repair, and scale-up in the new energy segment.

It believes that an improving growth outlook, combined with supportive valuations, sets the stage for a potential stock re-rating

According to its note, Reliance Retail has undergone a significant store rationalization process, with the closure of approximately 2,100 underperforming stores in fiscal 2025, and the cycle has now concluded.

It now expects the company to shift focus from aggressive expansion to quality growth.

Bernstein believes telecom will remain the bright spot as ARPU hike reflects in earnings, with moderating trends in capital expenditure.

Acceleration in Jio AirFiber rollout, faster broadband additions should drive growth in the segment, the note said.

As the brokerage revised its estimates post the final quarter results for fiscal 2025, it notes that the company is trading at a 15% discount to its three-year average valuation multiples based on projected earnings over the following 12-month period, making the risk-reward attractive.

JP Morgan On Reliance Industries

Maintain overweight stance with price target of Rs 1568 (earlier Rs 1530)

The brokerage believes that the next two years should be better than the last two for the company

A note released by the brokerage highlights the pressure that the stock has faced under large earnings cuts driven by weaker earnings in the refining and petchem segment.

JP Morgan believes that with the margins having fallen materially, there should be little sustained downside over the next fiscal period.

It believes that some cuts to Reliance Industries’ earnings are still possible, but should also be true for the rest of the market as well, making further underperformance unlikely.

. Read more on Markets by NDTV Profit.Bernstein and JP Morgan have raised their RIL target price, citing a new growth cycle, while Jefferies has gone for a minor trim. Read MoreMarkets, Notifications

NDTV Profit